Another Black Mark on September

The Dow Jones

Industrial Average has had 1016 triple digit

moves in its history, the first of which was

in 1987. While overall there are roughly the

same number of up days as down, today's loss

of 185.68 points makes September the month

with the greatest percentage of negative

triple digit moves. Two of the top three

biggest point drops of all time occurred in

September -

-

Sept

29, 2008: Dow drops 777.68

-

Oct 15, 2008: Dow drops

733.08

-

Sept

17, 2001: Dow drops 684.81

Of note, October

has the most triple digit moves in total.

Get

more September

stats here

Will 2010 Be as Good as 2009?

Tuesday December 29, 12:28 pm ET

By

Simon Maierhofer

John Templeton's observation that bull markets are born on pessimism,

grow on skepticism, mature on optimism and die on euphoria might never

have been more apropos than it is today.

There are

many pieces of Wall Street wisdom, some work, others don't, but John

Templeton's quote is one to remember. In fact, it may be the single most

important and most profitable principle for investors.

History

shows that this principle is as easily forgotten, as it is simple.

That's probably what makes it so effective. Investors, in particular

fund managers and analysts (more about that in a moment), should frame

John Templeton's advice and display it prominently, or use it as

screensaver.

The reason

we talk about investor sentiment is because it has reached extremes not

seen in years. Couple this with a 65% rally in the S&P (SNP: ^GSPC), Dow

Jones (DJI: ^DJI) and Nasdaq (Nasdaq: ^IXIC) and you have a possible

recipe for disaster.

A

bittersweet privilege

21st

century investors had the bittersweet privilege of eyewitnessing the

bust of several bubbles. Even though the bubbles all occurred in

different asset classes, they had one common denominator - sudden and

unexpected destruction.

A balloon

that has been punctured does not deflate in an orderly way. That has

been the case with technology (NYSEArca:

XLK -

News) in 2000, real estate (NYSEArca:

IYR -

News) following its 2005 top, and

the broad U. S. stock market (NYSEArca:

SCHB -

News), which topped in 2007 and

tumbled in 2008/2009.

If you are

one of the lucky few investors who foresaw all those asset bubbles,

there is no reason to continue reading, if you aren't, it might be a

good opportunity to reevaluate following the guidance that didn't keep

you out of asset bubbles.

2010 - On

the cusp

As 2009 is

winding down, various indicators have reached trigger levels not seen in

months, even years. None of those trusted gauges have bullish

implications. This means that 2010 might get off to a very rocky start.

The

Volatility Index (Chicago Options: ^VIX), also called VIX or fear index,

measures how concerned options traders are that prices will drop. As

with all sentiment indicators, the value of the VIX lies in its

contrarian application. For the first time since August 2008, the VIX

has now dropped below 20; a reading that has foreshadowed trouble in the

past.

Shortly

after this August 2008 extreme, the ETF Profit Strategy Newsletter

brand-marked the financial sector (NYSEARca:

XLF -

News) a 'downward spiral with no

stop-loss provision' and recommended short ETFs such as the UltraShort

Financial ProShares (NYSEArca:

SKF -

News) and UltraShort S&P 500

ProShares (NYSEArca:

SDS -

News).

Within six

months of the August VIX extreme, the S&P (NYSEArca:

SPY -

News) lost 45%, while financials

dropped over 75%.

Looking

back further, we notice that the VIX also fell below 20 in May 2008.

Just from May to August 2008, the S&P dropped 12%. Of course, the VIX

also fell below 20 in October 2007. We all know what happened

thereafter.

Be careful

who you trust

Most of us

look for a pro when it comes to matters beyond our knowledge. For a

health issue, we visit a physician, for car trouble we go to a mechanic,

etc. When it comes to investment guidance, however, trusting an advisor

may not be the best thing to do.

Investors

Intelligence is an organization that tracks about 140 financial

newsletters. In October 2007, 62% of the polled newsletter

writers/advisors thought prices would go up further. Only 19.6% were

bearish. The rest thought that the market would move higher after a

brief correction. We know today that 81.6% of those advisors were proven

wrong.

The

opposite happened in March 2009, when only 26.4% of the advisors were

bullish. This time, 73.6% were proven wrong. Going against the grain,

the ETF Profit Strategy Newsletter issued a strong buy alert on March

2nd. Stocks have rallied 65% since.

From

blessing to curse

What goes

up must come down. That pattern has been established by history and the

latter part (coming down) generally happens when least expected. This

65% rally from the March lows has morphed from blessing to curse. Now

that the profits have been reaped, all that this rally does is mortgage

2010 growth.

The above

Investors Intelligence and VIX readings show that the majority of

traders, investors, and advisors did not see any of the major market

turns coming since 2007. In fact, the vast majority of Wall Street has

been wrong-footed consistently.

Once

again, investors and advisors have set the stage for a major blindside.

The number of bulls tracked by Investors Intelligence has reached the

highest level since December 2007 while the number of bears clocked in

at the lowest level in over six years. This is in addition to the

message conveyed by the VIX.

The extent

of the damage

We

mentioned above the declines following extreme readings in October 2007,

May 2008 and October 2008. Each decline was different in character but

each lead to lower lows. October 2007 was followed by lower prices in

May 2008, which was followed by lower prices in September 2008.

The

rallies in between the above-mentioned secondary highs never advanced

beyond flash in the pan status and did nothing more than once again

trick investors into buying stocks at higher prices. Odds are, the rally

from the March low will become known as the biggest flash in the pan, or

sucker rally, since the Great Depression.

But, this

time is different

The most

fascinating facet of investment research is the consistent appearance of

the 'this time is different syndrome.' The market does what it's always

done, but every time a top of larger degree is upon us, we find excuses

for stocks to move even higher - just to be disappointed time and again.

If the

stock market were a person or entity, it would probably compare

investors to a poker player that falls again and again for the same

bluff. The best way to call your opponents bluff is by knowing his hand.

Well, here's what the stock market has in store for us.

Perception, to a large extent, is what drives the market, but perception

is not real. Perception, like a poker player's face (aka poker face) can

differ widely from the true value (aka the actual hand of cards).

If you

boil it down to the basics, you come up with this formula:

Valuation

+ Perception = Market Value

Obviously,

perception is the big fluctuating variable. Eventually, however, the

market will always disregard perception and reset the market to its

proper valuation. At that time the formula is: Market Value = Valuations

In other

words, your opponents poker face may be enough to up the ante for a

while, but when it comes time to settle the score, only what's in your

hand counts. The same is true for stocks. In the end, only true value

counts.

Calling a

bluff

With its

gravitation like pull, the market has a way of bringing stocks down to a

fair valuation level. This level can be measured by simple yet effective

indicators such as dividend yields and P/E ratios.

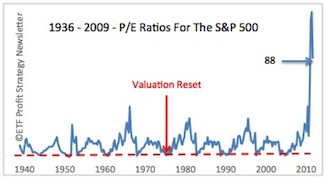

Major

market bottoms, such as in the 1920s, 1930s, 1950s, 1970s, and 1980s saw

P/E ratios drop to multi-decade lows while dividend yields rose to

multi-decade highs. Right now - and even nine months ago - P/E ratios

are the highest they've ever been, while dividend yields are close to

their 1999 all-time lows - the opposite of what you'd expect to see at a

market bottom.

The

November issue of the

ETF Profit Strategy Newsletter

includes a detailed historical analysis of P/E ratios, dividend yields,

and other reliable indicators plotted against current prices to

determine a target range for the ultimate market bottom. Indicative of

their implications, we've dubbed the indicators the 'Four Horsemen' -

yes, the March lows are in serious danger.

It may not

be apparent just yet, but the market is bluffing its way to higher

prices. The time to settle the score is speedily approaching. Will you

call the market's bluff and prepare for a major decline, or will you be

blindsided into holding stocks at the worst of times?

|